The first rule of panic is simple: "

Panic before everyone else does." With that rule in mind, the pertinent question at hand is also simple: "

Should I panic now?"

For those in Europe, I offer an emphatic "

Yes!" One is foolish at best to keep more than 100,000 euros in any European bank, especially any Southern European banks.

There is a clear and obvious "

Rational Reason to Panic".

By "panic" I mean get your money out now, while you can, before everyone else does. I am not the only one who thinks that way. Wolfgang Münchau makes a well-stated case in his Der Spiegel column

Euro rescue plan: Thank Dijsselbloem!Dutch Finance Minister and Euro Group Chief, Jeroen Dijsselbloem earned much criticism because he deviated from the official line that Cyprus was an "isolated incident".

I welcome this unusual burst of openness. Dijsselbloem expressed the brutal truth. I'm not criticizing that he states the policy. Rather, I criticize the policy itself.

This policy will destroy the euro, with the two now foreseeable interlocking mechanisms.

The first way is capital flight from the euro crisis countries. Expect permanent restrictions on the free movement of capital.

The second way is a never ending recession in the eurozone.

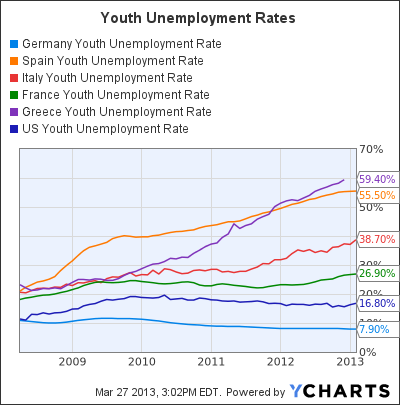

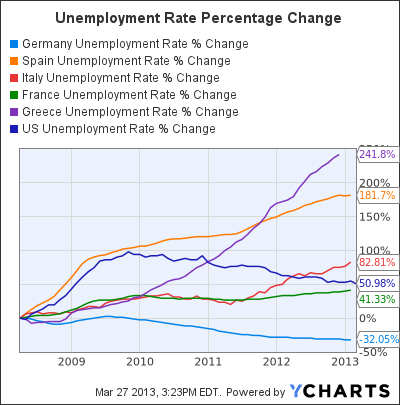

The first of these mechanisms is the logical consequence of Dijsselbloem's settlement blueprint. Spanish or Portuguese citizens would be pretty stupid to keep over 100,000 euros in a savings account.

Rational savers will distribute their assets to different banks, each with a limit of €100,000. German savers will do so as well.

Germany rejects a European deposit guarantee, so no credible reinsurance exists across southern Europe. Most of the Southern states are insolvent. A Cyprus-like rescue works only in context of a union of banks, and Germany emphatically rejects that mechanism.

Dijsselbloem's blueprint and Germany's veto of a European deposit guarantees savers have a "rational reason to panic now", everywhere.

The Withdrawal Debate Has Begun

US economist Paul Krugman says that it now is the best for Cyprus to leave the euro.

Cyprus is officially an "isolated incident". Greece, Spain, and Portugal will be there as well. Dijsselbloem's dictum guarantees that end. And Because there are proportionally fewer large savers in Spain than Cyprus, the hazard on a participation of small savers is even greater.

Expect bank runs or permanent controls on capital flows. Either way, the Monetary Union will come to an end.

Right for the Wrong Reasons Reader Bernd, from Germany, sent me the above link. I translated it, hopefully accurately, with a copy of this post going to Wolfgang Münchau.

In his email, Bernd says...

Paul Krugman has advised Cyprus to exit the Eurozone. You advised Cyprus the same, for the right reasons. Krugman does so, for the wrong reasons. I hope the day comes, when Münchau quotes you instead of Krugman.

Bernd

Hot Money BluesMünchau and Bernd refer to

Hot Money Blues by Paul Krugman.

Whatever the final outcome in the Cyprus crisis — we know it’s going to be ugly; we just don’t know exactly what form the ugliness will take — one thing seems certain: for the time being, and probably for years to come, the island nation will have to maintain fairly draconian controls on the movement of capital in and out of the country.

Depending on exactly how this plays out, Cypriot capital controls may well have the blessing of the International Monetary Fund, which has already supported such controls in Iceland.

It’s hard to imagine now, but for more than three decades after World War II financial crises of the kind we’ve lately become so familiar with hardly ever happened. Since 1980, however, the roster has been impressive: Mexico, Brazil, Argentina and Chile in 1982. Sweden and Finland in 1991. Mexico again in 1995. Thailand, Malaysia, Indonesia and Korea in 1998. Argentina again in 2002. And, of course, the more recent run of disasters: Iceland, Ireland, Greece, Portugal, Spain, Italy, Cyprus.

What’s the common theme in these episodes? Conventional wisdom blames fiscal profligacy — but in this whole list, that story fits only one country, Greece. Runaway bankers are a better story; they played a role in a number of these crises, from Chile to Sweden to Cyprus. But the best predictor of crisis is large inflows of foreign money: in all but a couple of the cases I just mentioned, the foundation for crisis was laid by a rush of foreign investors into a country, followed by a sudden rush out.

Now what? I don’t expect to see a wholesale, sudden rejection of the idea that money should be free to go wherever it wants, whenever it wants. There may well, however, be a process of erosion, as governments intervene to limit both the pace at which money comes in and the rate at which it goes out. Global capitalism is, arguably, on track to become substantially less global.

And that’s O.K. Right now, the bad old days when it wasn’t that easy to move lots of money across borders are looking pretty good.

85% RubbishAs is typically the case, Krugman gets part of the story correct, the sensational part (which helps explains his popularity). Everything else he says is generally rubbish.

Krugman is correct that Cyprus is going to be ugly. And he is sure to follow up with numerous "I told you so" articles when that happens.

This is where common sense stops and nonsense begins. Europe and the US do not suffer from lack of capital controls. The origin of this crisis is fractional reserve banking in and of itself.

The Krugman "solution" is more government controls, more taxation, more regulation, more manipulation, even to the point of actually advocating the "bad old days" when everyone had capital controls.

In addition to capital controls, Krugman advocates tariffs, advocates higher minimum wages, higher taxes, and more government spending.

Good grief!Money flows to places like Cyprus, Luxembourg, and Spain "because of " inane Keynesian and Monetarist programs elsewhere.

Not once does Krugman ever stop and think that the very policies that he espouses are precisely what has caused the capital flight!

Rather than address the root problems, Krugman now wants capital controls on top of all the other foolish things he desires.

When does it stop Paul? When?

Reflections on Münchau's Shift in AttitudeI believe Münchau's heart is in the right place. He really wanted to make the eurozone work, believing the euro would help create a better Europe.

However, the eurozone can never work. The euro was fatally flawed from the beginning, starting with a "

one size fits Germany" interest rate policy and lack of appropriate banking unions. The global recession brought those flaws to the forefront, and the North-South divide is the widest ever, and growing.

To no surprise (at least in this corner) euro skepticism is large and growing in the UK, Italy, Greece, and Poland. Cyprus and Spain will soon follow.

Meanwhile, attitudes in Germany and the Netherlands make it impossible for there ever to be the union that Münchau once envisioned.

It is extremely refreshing to see Münchau questioning ideas he once held sacrosanct. For that reason I commend Münchau, even though quoting Krugman for the wrong reasons can hardly be commended.

Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com

Wine Country ConferenceI am hosting an

economic conference on April 5 in Sonoma, California. Proceeds go to the Les Turner ALS Foundation (Lou Gehrig’s Disease).

Please see

My Wife Joanne Has Passed Away; Stop and Smell the Lilacs for my association with the disease.

To learn about the economic conference with world-class speakers including

John Hussman, Michael Pettis, Jim Chanos, John Mauldin, Mike “Mish” Shedlock, Chris Martenson with guest moderator Lauren Lyster and other Special Guests, please visit

Wine Country Conference April 5, 2013